Managing a deceased estate is rarely simple. Along with dealing with grief and family responsibilities, executors are often expected to handle complex financial and tax matters that many people have never dealt with before.

In Australia, executors are legally responsible for managing the tax obligations of the deceased estate. This may include lodging final tax returns, reporting estate income, handling capital gains tax, and ensuring the estate complies with Australian Taxation Office (ATO) requirements.

Unfortunately, many executors make mistakes during the administration process without realising the long-term consequences. Even small errors can lead to delays, penalties, disputes between beneficiaries, or unnecessary tax liabilities.

Understanding the most common tax mistakes executors make with deceased estates can help families avoid complications and manage estate administration more confidently.

Understanding Tax Responsibilities for Deceased Estates

When someone passes away, their tax obligations do not automatically end. In many cases, the estate itself becomes a separate taxable entity until all assets are distributed.

Executors may need to:

- lodge the deceased person’s final tax return

- apply for a Tax File Number (TFN) for the estate

- report ongoing estate income

- manage capital gains tax obligations

- maintain financial records for the ATO

Depending on the size and complexity of the estate, this process can continue for months or even years.

Because estate taxation involves strict compliance rules, proper planning is extremely important from the beginning.

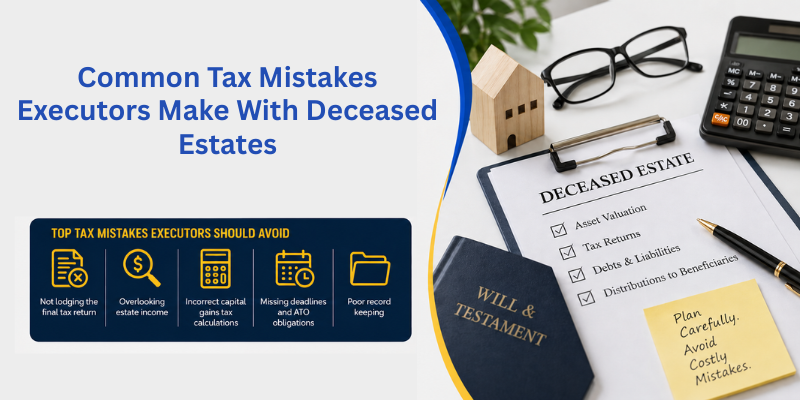

1: Failing to Lodge Final Tax Returns

One of the most common mistakes executors make is assuming tax obligations stop after death.

The deceased person’s final individual tax return still needs to be lodged for the period from:

- 1 July to the date of death

This final return may include:

- salary and wages

- investment income

- rental income

- business income

- capital gains events

Missing this requirement can create delays in estate administration and trigger ATO compliance issues later.

2: Overlooking Ongoing Estate Income

Many estates continue generating income after death.

This may include:

- rental income

- bank interest

- share dividends

- trust distributions

- business profits

Executors sometimes assume this income belongs directly to beneficiaries. However, during administration, the estate itself may need to lodge separate tax returns reporting this income.

Failing to report estate income correctly can lead to:

- penalties

- amended assessments

- beneficiary reporting issues

- ATO audits

Good record keeping is essential throughout the administration period.

3: Not Applying for a Separate TFN for the Estate

If the estate earns ongoing income, executors may need to apply for a separate TFN for the deceased estate.

This TFN is commonly required for:

- estate bank accounts

- investment reporting

- tax lodgements

- financial transactions

Some executors continue using the deceased person’s TFN incorrectly, which can create reporting problems later.

A separate estate TFN helps keep financial records organised and simplifies compliance obligations.

4: Incorrect Capital Gains Tax Calculations

Capital gains tax (CGT) is one of the most misunderstood areas of deceased estate administration.

Australia does not have inheritance tax, but CGT may still apply when inherited assets are sold.

Executors often make mistakes involving:

- property valuations

- cost base calculations

- exemption rules

- investment assets

- timing of property sales

These errors can significantly increase tax liabilities for beneficiaries.

Professional advice is especially important when estates involve:

- investment properties

- shares

- managed funds

- businesses

- multiple beneficiaries

Many families seek advice from an accountant in perth before selling inherited assets to avoid costly CGT mistakes.

5: Distributing Assets Too Early

Some executors distribute estate assets before all tax liabilities have been finalised.

This can become a major problem if:

- the ATO later issues additional assessments

- debts remain unpaid

- capital gains obligations arise

- estate income was not fully reported

Executors may become personally liable for unpaid tax obligations if assets are distributed prematurely.

Before making distributions, executors should ensure:

- tax returns are lodged

- liabilities are confirmed

- estate debts are resolved

- financial records are complete

Patience during the administration process often prevents bigger problems later.

6: Poor Record Keeping

Executors are responsible for maintaining proper records relating to the estate.

Unfortunately, record keeping is often overlooked during emotionally stressful situations.

Important records may include:

- bank statements

- property valuations

- share transactions

- beneficiary payments

- trust distributions

- legal expenses

- tax returns

Poor documentation can make it difficult to:

- calculate tax correctly

- respond to ATO requests

- resolve disputes

- finalise the estate efficiently

Good organisation from the beginning makes estate administration much smoother.

7: Ignoring Property Valuations

Date-of-death property valuations are critical for future CGT calculations.

Executors sometimes delay obtaining valuations or rely on informal estimates instead of professional appraisals.

This can create problems when:

- inherited property is sold later

- beneficiaries dispute asset values

- capital gains calculations are required

Accurate valuations help establish the correct cost base and reduce the risk of future tax complications.

8: Not Understanding Beneficiary Tax Obligations

Beneficiaries may also have tax obligations depending on:

- estate income distributions

- capital gains allocations

- trust structures

- inherited investments

Executors should provide clear records to beneficiaries so they can meet their own tax obligations correctly.

Confusion often occurs when estates involve:

- investment portfolios

- family trusts

- business interests

- rental properties

Professional guidance can help avoid misunderstandings between executors and beneficiaries.

9: Failing to Understand Trust and Estate Structures

Some deceased estates involve complex family trust arrangements.

Executors may struggle to understand:

- trust distributions

- beneficiary entitlements

- trust tax rules

- reporting requirements

Mistakes involving trust structures can trigger:

- additional tax liabilities

- beneficiary disputes

- compliance issues

In these situations, working with a Deceased Estate accountant perth professional experienced in estate taxation and trust compliance can help reduce risks significantly.

10: Delaying Professional Advice

Many executors wait until problems arise before seeking professional assistance.

Unfortunately, delayed advice often leads to:

- avoidable tax liabilities

- missed deadlines

- reporting mistakes

- delayed estate finalisation

Seeking guidance early in the administration process can help executors:

- stay organised

- understand obligations

- reduce stress

- avoid costly errors

Even relatively simple estates can become complicated when investments, trusts, or property assets are involved.

Capital Gains Tax Is Often the Biggest Challenge

One of the areas executors struggle with most is capital gains tax.

CGT commonly applies when:

- inherited property is sold

- shares increase in value after death

- investment assets are transferred or disposed of

However, certain exemptions may apply depending on:

- how the property was used

- ownership history

- the timing of the sale

- beneficiary arrangements

Because CGT rules can be highly technical, many executors benefit from professional tax guidance before selling inherited assets.

Why Executors Should Stay Organised

Estate administration often takes longer than people expect.

Some estates remain active for several years due to:

- property sales

- legal disputes

- trust structures

- business interests

- ongoing investment income

Staying organised throughout the process can help executors avoid unnecessary stress and delays.

Simple steps such as:

- maintaining clear records

- keeping separate estate accounts

- tracking income and expenses

- communicating regularly with beneficiaries

can make a major difference.

Tips to Avoid Common Estate Tax Mistakes

Executors can reduce risks by:

- applying for probate early

- obtaining professional valuations

- organising financial records immediately

- seeking tax advice before selling assets

- lodging returns on time

- keeping detailed beneficiary records

Taking a careful and methodical approach usually leads to smoother estate administration.

Final Thoughts

Managing a deceased estate involves far more than simply distributing assets to beneficiaries. Executors are responsible for handling tax returns, estate income, capital gains obligations, and ongoing ATO compliance requirements.

Unfortunately, many executors make avoidable mistakes because they underestimate how complex estate taxation can become. Errors involving capital gains tax, estate income reporting, beneficiary distributions, or record keeping can create significant financial and legal complications later.

Understanding these common tax mistakes can help executors manage the administration process more confidently and reduce unnecessary stress during an already emotional time.

For estates involving property, trusts, investments, or multiple beneficiaries, professional financial guidance can often save time, reduce tax risks, and help ensure everything is handled correctly from the beginning.