Retirement planning is no longer something you can postpone until your 50s. With rising living costs and increasing life expectancy, building a strong financial foundation early is essential. When comparing EPF vs PPF, many investors look for a secure and reliable way to save for retirement. The Employees’ Provident Fund (EPF) and the Public Provident Fund (PPF) are two of the most trusted government-backed retirement schemes in India.

The EPF vs PPF comparison highlights that while both investment options help individuals accumulate wealth over time, they cater to different types of investors and serve different financial needs. Understanding EPF vs PPF, including how each scheme works, their benefits, and their eligibility criteria, will help you choose the right retirement plan or even decide whether investing in both is the best strategy for achieving your long-term financial goals.

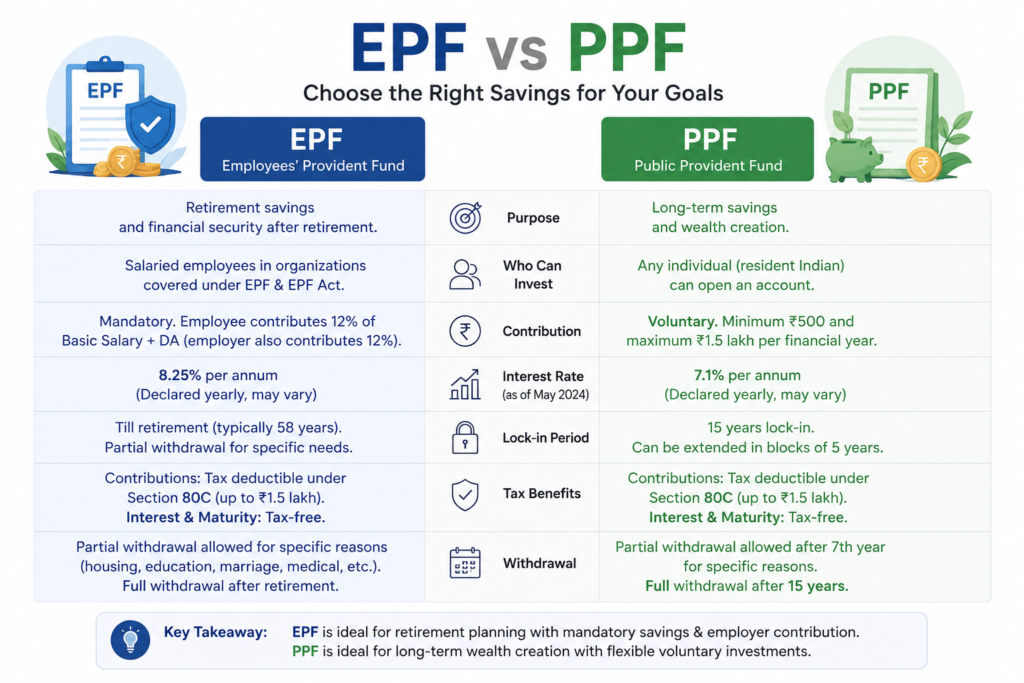

Understanding EPF

The Employees’ Provident Fund (EPF) is a mandatory retirement savings scheme for eligible salaried employees in India. Managed by the Employees’ Provident Fund Organisation (EPFO), it encourages disciplined savings by deducting a fixed percentage of an employee’s salary every month. Employers also contribute an equal amount, making EPF one of the most rewarding retirement benefits available to salaried professionals.

The accumulated balance earns annual interest declared by the government and continues to grow through the power of compounding. Employees can partially withdraw funds under certain circumstances, including purchasing a home, medical emergencies, children’s education, or marriage expenses.

Benefits of EPF

- Employer contribution increases retirement savings.

- Automatic monthly deductions encourage disciplined investing.

- Government-backed security.

- Attractive long-term interest rates.

- Tax deductions available under Section 80C.

- Partial withdrawal facility for specific financial needs.

Understanding PPF

The Public Provident Fund (PPF) is a voluntary long-term investment scheme introduced by the Government of India. Unlike EPF, it is available to everyone, including salaried employees, freelancers, self-employed professionals, business owners, and homemakers.

PPF allows investors to contribute any amount within the prescribed annual limit, making it highly flexible. The account has a maturity period of 15 years, although investors can extend it in five-year blocks after maturity.

One of the biggest advantages of PPF is its tax-efficient nature, where investments, interest earned, and maturity proceeds are generally tax-free under applicable rules.

Benefits of PPF

- Open to all Indian residents.

- Flexible annual investment options.

- Completely government-backed.

- Suitable for long-term wealth creation.

- Tax-saving investment under Section 80C.

- Tax-free interest and maturity amount.

EPF vs PPF: Key Comparison

Eligibility

EPF is available only to eligible salaried employees, while PPF can be opened by almost every Indian resident regardless of employment status.

Investment Method

EPF contributions are automatically deducted from your monthly salary along with employer contributions. PPF investments are voluntary, allowing investors to deposit funds whenever convenient during the financial year.

Retirement Corpus

EPF generally builds a larger retirement corpus because both the employee and employer contribute regularly. PPF relies solely on individual investments, making disciplined contributions essential.

Withdrawal Rules

EPF offers greater flexibility for partial withdrawals under approved conditions. PPF has stricter withdrawal rules, allowing limited withdrawals after a specified number of years.

Risk Factor

Both EPF and PPF are considered among the safest investment options because they are backed by the Government of India. They are ideal for conservative investors seeking stable and predictable returns.

Who Should Invest in EPF?

EPF is best suited for salaried employees who receive employer contributions. Since contributions happen automatically every month, it becomes easier to accumulate retirement savings without requiring active investment decisions.

Employees who remain invested throughout their careers can build a substantial retirement fund with minimal effort.

Who Should Invest in PPF?

PPF is an excellent choice for self-employed individuals, freelancers, entrepreneurs, and anyone looking for a secure long-term investment. It is also suitable for salaried employees who have already invested in EPF but want to create an additional retirement corpus.

Parents often open PPF accounts for their children to support future educational or financial goals.

Can You Invest in Both?

Yes. In fact, many financial planners recommend investing in both EPF and PPF whenever possible.

EPF provides retirement security through salary-based contributions and employer support, while PPF offers an additional avenue for tax-efficient, long-term savings. Together, they help diversify retirement planning and reduce dependence on a single investment source.

Final Verdict

There is no universal winner in the EPF vs PPF debate because the right choice depends on your employment status, financial goals, and investment preferences.

If you are a salaried employee, EPF should form the foundation of your retirement planning due to employer contributions and automatic savings. If you are self-employed or looking to strengthen your retirement portfolio further, PPF offers unmatched flexibility and government-backed security.

For long-term financial stability, combining EPF with PPF can provide a balanced retirement strategy that delivers disciplined savings, tax benefits, and peace of mind for the future.