Fixed deposits have long been one of the most popular savings and investment options among individuals seeking stability, predictable returns, and capital protection. Whether you are a first-time saver, a young professional building an emergency fund, or someone looking to diversify your investment portfolio, a fixed deposit (FD) offers a simple way to grow your money without taking on significant market risk.

However, many investors focus only on the advertised FD interest rates when choosing a deposit. While interest rates are undoubtedly important, they do not always tell the complete story. The actual amount you earn depends on several factors, including the deposit tenure, compounding frequency, investment amount, and the type of payout selected.

This is where a fixed deposit calculator becomes valuable. Instead of making rough estimates, you can accurately calculate your maturity value and understand your real returns before investing. By using a calculator, you can compare different interest rates, tenures, and deposit amounts to make more informed financial decisions.

In this guide, we explain how FD interest rates work, how a fixed deposit calculator helps estimate returns, and how you can use it to maximise the value of your savings.

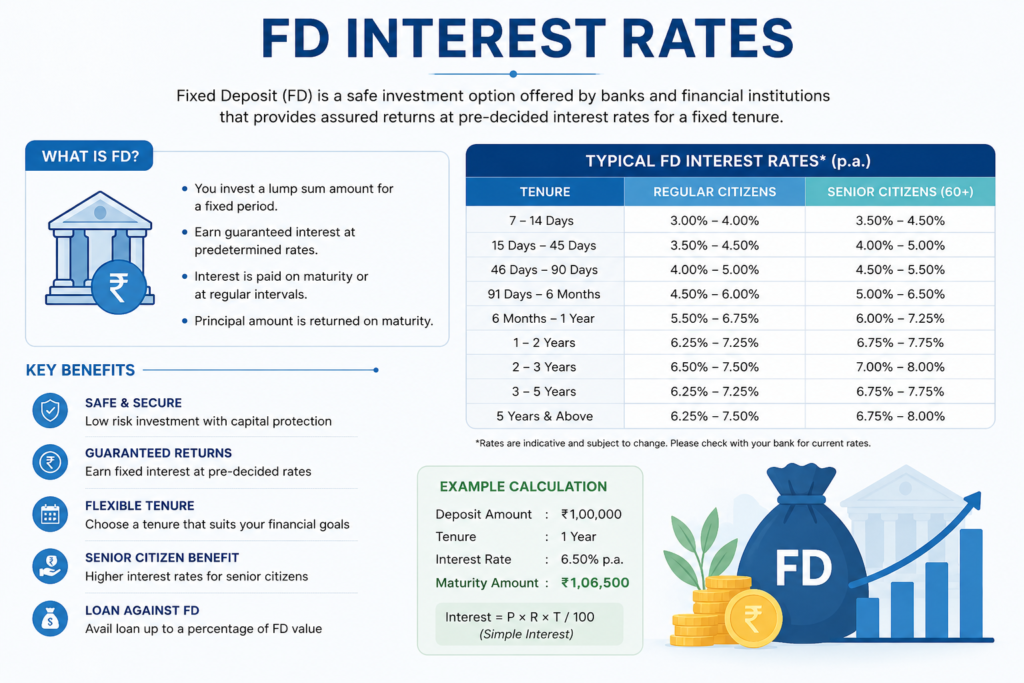

Understanding FD interest rates

An FD interest rate represents the percentage return offered on the amount deposited for a specific tenure. Financial institutions generally provide different rates depending on the duration of the deposit. Longer tenures may sometimes offer higher rates, although this is not always the case.

The interest earned on an FD is influenced by:

- The principal amount invested

- The applicable interest rate

- The deposit tenure

- The compounding frequency

- The payout option selected

Even a small difference in interest rates can significantly impact the final maturity amount, particularly when investing larger sums or choosing longer tenures.

For example, a difference of one percentage point may appear minor initially. However, when compounded over several years, the additional earnings can become substantial. Therefore, comparing interest rates carefully before investing is essential.

Why advertised interest rates do not reveal your actual returns

Many investors assume that the highest advertised interest rate automatically results in the best returns. In reality, several additional factors influence the final outcome.

Consider the following situations:

Different tenures

An FD offering a slightly lower interest rate over a longer tenure may generate higher overall returns compared to a shorter-term deposit with a higher rate.

Compounding frequency

Interest may be compounded monthly, quarterly, half-yearly, or annually. More frequent compounding generally leads to higher returns because interest is earned on previously accumulated interest.

Interest payout options

Some deposits provide periodic interest payouts, while others reinvest the earned interest. Reinvestment often results in greater maturity values due to compounding.

Investment amount

Larger deposits naturally generate more interest income, making it important to understand how your chosen amount affects final returns.

Because multiple variables influence earnings, relying solely on interest rates can lead to inaccurate expectations. A fixed deposit calculator helps eliminate this uncertainty.

What is a fixed deposit calculator?

A fixed deposit calculator is an online financial tool designed to estimate the maturity value and interest earnings of an FD investment.

Instead of manually calculating compound interest formulas, investors can simply enter a few details and instantly receive an estimate of:

- Total investment amount

- Interest earned

- Maturity value

- Periodic income, where applicable

The calculator provides clarity before making an investment decision and allows users to compare various scenarios quickly.

It is especially useful for first-time investors who may not be familiar with compound interest calculations.

How a fixed deposit calculator works

Most FD calculators require the following inputs:

Principal amount

This refers to the initial amount invested in the fixed deposit.

Interest rate

The annual rate offered on the deposit.

Investment tenure

The duration for which funds will remain invested.

Compounding frequency

The frequency with which interest is added to the principal.

Once these details are entered, the calculator automatically estimates the maturity value and total interest earned.

The process typically takes only a few seconds and removes the need for manual calculations.

Example: Understanding real returns with an FD calculator

Suppose a young professional decides to invest £5,000 equivalent in a fixed deposit.

The investor enters:

- Principal amount: £5,000

- Interest rate: 7%

- Tenure: 3 years

- Quarterly compounding

The calculator immediately displays:

- Initial investment

- Total interest earned

- Final maturity amount

The investor can then modify the tenure or interest rate to see how returns change under different scenarios.

For example, increasing the tenure to five years may significantly increase the maturity value due to the power of compounding.

Similarly, comparing a 6.5% interest rate against a 7% interest rate helps illustrate the long-term impact of even small changes.

Comparing different FD interest rates using a calculator

One of the biggest advantages of a fixed deposit calculator is the ability to compare multiple investment options.

Scenario 1: Lower rate, shorter tenure

An investor chooses a two-year FD with a moderate interest rate.

Scenario 2: Higher rate, longer tenure

The same investor explores a four-year FD offering a slightly higher rate.

The calculator helps compare:

- Total interest earned

- Maturity values

- Effective annual returns

This comparison enables investors to select the option that best aligns with their financial goals.

Without a calculator, these comparisons can become complicated and time-consuming.

The role of compounding in FD returns

Compounding is one of the most powerful factors affecting fixed deposit returns.

When interest is compounded, earned interest gets added to the principal. Future interest calculations are then based on the increased balance.

As a result, investors earn interest on both:

- The original principal

- Previously earned interest

Over longer periods, this can substantially increase the maturity amount.

For example, two FDs with identical interest rates may generate different returns if one compounds quarterly and the other compounds annually.

A fixed deposit calculator highlights these differences clearly and helps investors understand the benefits of reinvested earnings.

Choosing the right tenure for your financial goals

Different financial objectives require different FD tenures.

Short-term goals

Individuals saving for:

- Holidays

- Consumer purchases

- Emergency funds

may prefer shorter deposit tenures.

Medium-term goals

Investors planning for:

- Higher education

- Home renovations

- Business expansion

may consider medium-duration deposits.

Long-term goals

Longer tenures may suit individuals building wealth gradually while benefiting from compounding.

A calculator helps determine which tenure provides the most suitable balance between liquidity and returns.

Benefits of using a fixed deposit calculator

Accurate planning

Investors can estimate future earnings with greater precision.

Quick comparisons

Multiple FD options can be analysed within minutes.

Better decision-making

Understanding maturity values helps investors choose appropriate tenures and deposit amounts.

Goal-based investing

Calculators help determine how much needs to be invested to achieve a future financial target.

Improved financial confidence

Knowing the likely returns before investing reduces uncertainty and helps investors plan more effectively.

Common mistakes to avoid when evaluating FD returns

Looking only at the interest rate

Interest rates are important but should not be the sole decision-making factor.

Ignoring compounding

Compounding frequency significantly influences final returns.

Choosing unsuitable tenures

Selecting a tenure without considering future liquidity requirements may create financial challenges.

Not comparing options

Failing to compare multiple FD scenarios can result in missed opportunities.

Overlooking maturity values

The final maturity amount often provides a better picture than focusing only on annual interest rates.

Using a fixed deposit calculator helps investors avoid these common mistakes.

How first-time savers can benefit from FD calculators

Young professionals and first-time savers often begin their investment journey with limited experience.

A fixed deposit calculator provides a practical way to understand:

- How interest accumulates over time

- The impact of different tenures

- The benefits of compounding

- The relationship between investment amount and maturity value

This knowledge can help build strong saving habits and encourage more disciplined financial planning.

By experimenting with different scenarios, new investors gain confidence in making informed investment decisions.

Conclusion

Fixed deposits remain one of the simplest and most reliable ways to grow savings while preserving capital. However, understanding FD interest rates alone is not enough to determine the actual value of an investment. Factors such as tenure, compounding frequency, investment amount, and payout options all influence the final returns.

A fixed deposit calculator bridges this knowledge gap by providing a clear picture of expected earnings before any money is invested. It allows investors to compare options, assess different scenarios, and identify the most suitable strategy for their financial goals.

Whether you are opening your first FD or planning a larger investment, using a fixed deposit calculator can help you move beyond advertised interest rates and focus on what truly matters—your real returns.