The Strategic Shift Toward Outsourcing in Commercial Lending

In 2026, the global banking landscape is undergoing a structural transformation driven by digital acceleration, margin pressures, and evolving borrower expectations. Commercial lending, once heavily reliant on in-house expertise and legacy systems, is now being reimagined through strategic partnerships. As the market expands rapidly—projected to exceed $11 trillion in 2026—banks are increasingly adopting commercial lending outsourcing as a means to stay competitive and agile.

This shift is no longer about cost-cutting alone. It reflects a broader move toward operational resilience, technological advancement, and scalable growth.

Cost Optimization Meets Operational Efficiency

One of the primary drivers behind outsourcing is the need to manage costs in an environment of tightening margins. Banks are under pressure to streamline operations while maintaining service quality. Outsourcing enables financial institutions to significantly reduce operational overhead while improving process efficiency and turnaround times.

By delegating non-core and process-heavy functions such as loan processing, underwriting support, and documentation management, banks can reallocate internal resources toward higher-value activities like relationship management and portfolio strategy. In 2026, cost efficiency is no longer a periodic initiative but a continuous operational priority embedded into the banking model.

Access to Specialized Expertise and Advanced Technology

Modern commercial lending is increasingly complex, requiring expertise in data analytics, regulatory compliance, and risk modeling. Building these capabilities internally is both time-consuming and expensive. Strategic outsourcing partners bring domain expertise and advanced technologies, including AI-driven credit assessment and automated underwriting tools.

This access enables banks to modernize their lending operations without large upfront investments. It also ensures faster adoption of innovations such as real-time risk analysis and predictive portfolio management, which are becoming essential in a competitive lending environment.

Accelerating Digital Transformation and Speed to Market

Speed has become a critical differentiator in commercial lending. Borrowers increasingly expect faster approvals, seamless onboarding, and real-time decision-making. Traditional lending processes, often constrained by legacy systems, struggle to meet these expectations.

Outsourcing partners help banks digitize workflows, integrate APIs, and implement automated systems that reduce loan origination cycles. This aligns with broader 2026 banking trends focused on removing friction, shortening decision cycles, and enhancing data accuracy across digital channels.

As a result, banks can deliver quicker credit decisions and improved customer experiences, reducing the risk of losing clients to more agile competitors such as fintechs and alternative lenders.

Enhancing Scalability and Flexibility

Commercial lending volumes are subject to market fluctuations, regulatory changes, and economic cycles. Maintaining a fixed in-house workforce to handle variable demand can lead to inefficiencies. Outsourcing introduces a flexible operating model that allows banks to scale operations up or down as needed.

This scalability is particularly valuable in periods of rapid growth or economic uncertainty. With outsourcing partners handling capacity surges, banks can maintain consistent service levels without overextending internal teams.

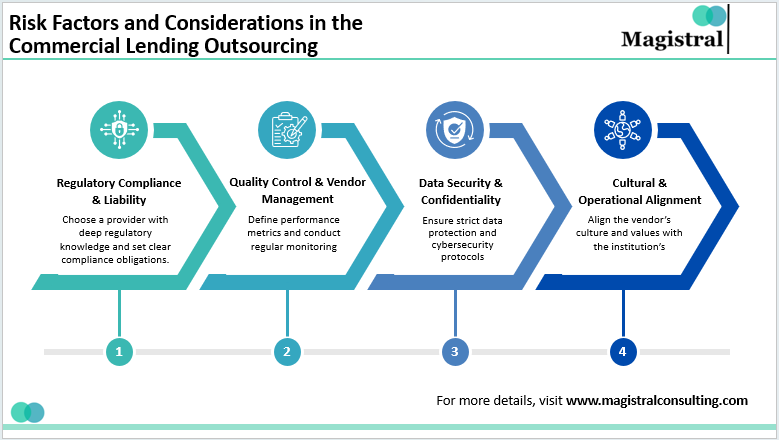

Strengthening Risk Management and Compliance

Regulatory requirements in commercial lending continue to grow more complex. From credit risk assessments to compliance reporting, banks must ensure accuracy and transparency at every stage of the lending lifecycle.

Outsourcing providers often specialize in regulatory processes and maintain updated compliance frameworks. Their use of advanced analytics and automated controls helps reduce errors, improve audit readiness, and enhance overall risk management. Additionally, predictive tools enable early identification of portfolio risks, allowing proactive mitigation strategies.

From Vendor Relationships to Strategic Partnerships

The nature of outsourcing itself is evolving. Banks are no longer engaging vendors solely for transactional support. Instead, they are forming long-term strategic partnerships focused on innovation, co-creation, and continuous improvement.

In 2026, outsourcing is seen as a strategic lever that enables banks to combine internal strengths with external capabilities. This collaborative approach allows institutions to remain competitive in a rapidly changing ecosystem shaped by digital disruption, talent shortages, and rising customer expectations.

Conclusion: A Core Component of Future-Ready Lending

Commercial lending is at a pivotal moment where efficiency, speed, and innovation determine success. Outsourcing has emerged as a critical enabler, helping banks transform legacy operations into agile, technology-driven ecosystems.

As financial institutions navigate increasing complexity and competition, strategic partnerships will play a central role in shaping the future of lending. Rather than a supporting function, outsourcing is becoming a core component of how banks design, deliver, and scale commercial lending in 2026 and beyond.